Grant’s Go-To’s: SFRP’s Aim at Target Date Funds as Default Investment Option

Recent editions of this column have examined key design decisions that are part of the process of developing of state-facilitated retirement savings programs (SFRP) – e.g., whether the program will be an auto-IRA, a MEP, a marketplace (or some combination thereof); whether employer participation will be required; and, whether to adopt automatic enrollment and escalation features.

Another important decision has to do with the investment options that will be made available, and how contributions of workers who do not make an affirmative choice will be invested. These decisions are generally made closer to program launch, and in consultation with a record keeper and investment and other consultants.

Determining the “default” investment for savers who do not make a decision about where to direct their contributions is a weighty decision. The downside of putting the money into investments that carry more risk, and a greater potential for loss, is obvious. But parking the contributions in a “safe” investment with lower risk means participants’ accounts may not grow sufficiently to provide significant income security in retirement. Increasingly, target-date funds (TDFs) have become a popular solution.

TDFs, which are included in the Department of Labor’s definition of a Qualified Default Investment Alternative, are generally pegged to a person’s age and/or likely date of retirement. The funds are designed to reduce exposure to risk over time in a manner that coincides with participants’ decreasing tolerance for risk over the course of their careers. According to Vanguard, 94 percent of defined contribution plans include TDFs, and 54 percent of participants hold a TDF as their sole investment.

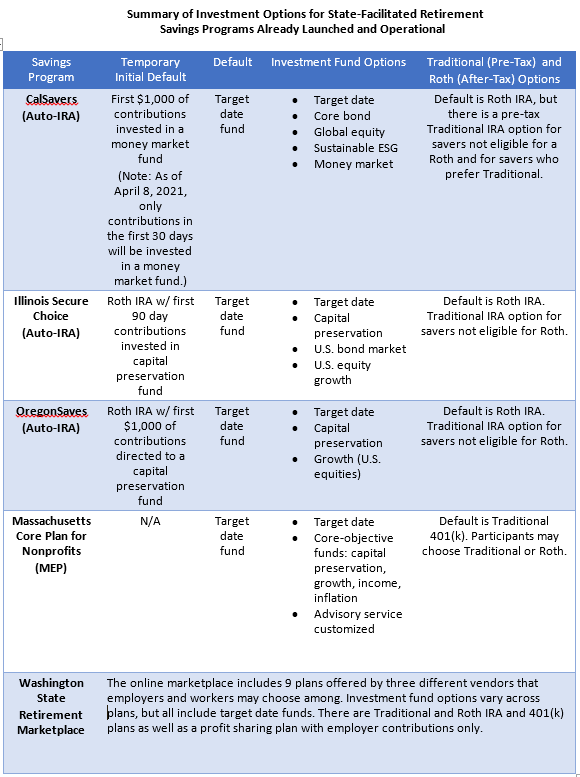

As is evident in the table below, TDFs appear to have already gained a prominent place in state-facilitated programs.

California, Illinois and Oregon each have an initial period where contributions are directed to a money market or capital preservation fund until a specific threshold of time or dollars contributed is reached. In response to the current low interest rate environment, the CalSavers Board recently acted to change the program’s threshold to more quickly direct contributions to the TDFs beginning in April 2021.

The table also shows that with the exception of the Massachusetts Core Plan, after-tax Roth funds are emerging as the most common default option. After-tax savings options may well be better suited for SFRP participants as workers with lower incomes don’t enjoy the advantages of pre-tax savings to the same extent as workers with higher incomes.

Illinois Secure Choice and OregonSaves offer a Traditional IRA option only to participants who need to re-characterize their contributions because their incomes make them ineligible for Roth IRAs. CalSavers makes the option available to all savers.

For more information about investment options adopted by programs already launched and operating, here are links to webpages that provide more details: CalSavers; Illinois Secure Choice; OregonSaves; Massachusetts Core Plan for Nonprofits; Washington State Retirement Marketplace.

What’s on tap for next time? As the first state-facilitated programs begin to mature a bit and more and more states have programs in development, I’ve been thinking a lot about how we might measure success. I plan to share some of my thoughts on that.

Stay tuned! - Grant

This piece was featured in the March 25, 2021 edition of Retirement Security Matters. For more fresh thinking on retirement savings innovation, and for a shot of John shucking oysters, check out the newsletter here.